The Death of Gray-Market DDP: Decoding Trump’s June 3 Executive Order on US Customs Enforcement and the New Foreign IOR Restrictions

On June 3, 2026, the operational landscape for cross-border brands, supply chain managers, and logistics networks underwent a permanent structural transformation. U.S. President Trump officially signed an aggressive, wide-ranging executive order titled “Strengthening Customs Enforcement.”

This directive is not a routine administrative patch or a minor software update to the Automated Commercial Environment (ACE) portal. It is a calculated, regulatory clampdown specifically aimed at dismantling the Foreign Importer of Record (FIOR) customs clearance framework. For years, offshore enterprises and e-commerce platforms have relied on this mechanism to orchestrate low-cost imports into the United States.

If your brand currently relies on traditional “all-inclusive customs clearance and tax-paid” services (commonly marketed as gray-market DDP sea or air freight), or if your business model utilizes a foreign-registered corporation to execute US customs entries, your supply chain is now standing in an immediate regulatory crosshair. The windows for compliance mitigation are closing rapidly.

Below is an extensive, data-driven operational breakdown of the executive order, the mechanical shifts in U.S. Customs and Border Protection (CBP) enforcement protocols, and the concrete strategies required to insulate your cargo from systemic seizures, liquidating damages, and port liquidations over the next 90 to 180 days.

1. The Anatomy of the Order: Why the US is Targeting Foreign Importers

To understand the severity of this enforcement wave, you must look at how CBP evaluates risk. Under conventional international trade frameworks, a foreign entity is legally permitted to act as an Importer of Record (holding an importer number starting with a country code, such as “99-“). However, from an enforcement standpoint, CBP has long viewed the Foreign IOR model as an unmitigated structural liability.

When an offshore entity with zero physical assets, no U.S.-based bank accounts, and no domestic corporate officers violates trade laws, CBP has no financial lever to pull. If that importer under-declares cargo values, utilizes incorrect Harmonized Tariff Schedule (HTS) classifications, or evades Section 301 punitive tariffs, collecting unpaid duties, anti-dumping fees, or civil penalties becomes nearly impossible once the cargo clears the port gate.

THE NEW CBP COMPLIANCE VERIFICATION MATRIX

| Compliance Metric | Legacy FIOR System (Pre-2026) | Post-June 3 Executive Order |

| Entry Profile Eligibility | Section 321 / Type 86 Allowed | Formal Entry Only (Type 01/11) |

| Bond Structuring | Multi-Use Continuous Bonds | Single Transaction Bonds (STB) |

| Asset Verification | None Required (Offshore Paper) | Verifiable Domestic Assets |

| Customs Valuation Audit | Pro Forma Commercial Invoice | Mandated Export Declarations |

| Discretionary Penalty Relief | Case-by-Case Mitigation | 50% Statutory Minimum Floor |

To eliminate this enforcement blind spot, the June 3 Executive Order systematically strips away the privileges previously granted to foreign-registered importers. It establishes rigorous new baseline parameters for any organization executing a customs entry for goods shipping from China to the US.

New Baseline Mandates for All Registered Importers:

- Tangible Asset Deficits & Bond Ramping: All IORs must now demonstrate a verified threshold of tangible financial assets physically located within U.S. jurisdictions. If an importer cannot satisfy these asset verification metrics, CBP will automatically mandate an aggressive scaling of their basic bond values.

- Exhaustive Corporate Disclosure: Importers are now legally obligated to file an granular corporate transparency manifest. This includes verified projections of historical and forward-facing import volumes, accurate years of active incorporation, ultimate beneficial owner (UBO) identities, cross-border corporate parent-subsidiary affiliations, and explicit ledgers of domestic financial accounts.

- The “Good Standing” Registry: CBP is launching a real-time, centralized database tracking importer compliance records. Any entity linked to persistent HTS misclassifications, late filings, or unresolved valuation challenges will be demoted to “Not in Good Standing.” This classification triggers an automatic, systemic freeze on their ability to file customs entries or operate as an authorized IOR at any U.S. port of entry.

The Bottom Line: In plain English, if you don’t have a real corporate footprint or verifiable assets inside the US, customs will now treat your cargo as high-risk by default. No more hiding behind a foreign registration.

2. Increased Broker Liability: The End of “Blind Clearance”

A critical, often overlooked mechanism within this executive order is the secondary enforcement layer applied directly to licensed U.S. customs brokers and international freight forwarders.

Historically, some high-volume customs brokers would process thousands of automated entries daily for foreign freight forwarders, doing little to no independent verification of the actual shipper or the validity of the declared values. The June 3 order permanently closes this loophole by making customs brokers legally and financially co-responsible for the compliance health of their clients.

The New Mandates Enforced on U.S. Customs Brokers Include:

- Strict Know-Your-Customer (KYC) Protocols: Brokers must independently verify the physical office locations, operational legitimacy, and banking footprints of the foreign entities they represent.

- Mandatory Proactive Inquiries: If a broker processes an entry where the declared commercial value sits noticeably below the statistical average for that specific HTS code, the broker can no longer claim ignorance. They are required to actively demand verifiable cost sheets, factory proof-of-payment logs, and production contracts before submitting the entry to the ACE portal.

- Maximum Penalty Enforcement: Brokers who fail to execute these due diligence screens face catastrophic administrative fines, immediate loss of their corporate customs licenses, and direct exposure to the financial liabilities of the non-compliant foreign importer.

As a direct consequence, reputable, licensed U.S. customs brokers are rapidly offloading high-risk foreign accounts. If your current forwarder relies on a broker network that lacks rigid, professional compliance screening, your containers run an immediate risk of getting stranded at the terminal simply because no licensed broker is willing to sign off on the manifest.

3. Three Structural Restrictions Effectively Liquidating the Foreign IOR Model

For companies heavily involved in importing from China to the US, the executive order outlines three specific operational changes that remove the economic viability of utilizing an offshore corporate entity for customs processing.

I. Total Prohibition of Informal Entry Pathways

The most immediate, painful blow to high-volume cross-border platforms is the explicit ban preventing Foreign IORs from accessing informal entry mechanisms. Effective immediately, foreign-registered corporate entities are completely barred from utilizing:

- Section 321 De Minimis Exemptions: Duty-free entry processing for shipments with a fair retail value under $800.

- Type 86 Quick Clearance Entries: The automated filing system widely used by air-express integrators and consolidation lines to clear millions of low-value e-commerce packages daily.

All cargo cleared under a Foreign IOR profile must now be routed exclusively through Formal Entry Procedures (Entry Type 01 or Type 11), irrespective of the item’s actual unit value. This shifts an immense administrative and financial burden onto the importer, forcing them to pay standard harbor maintenance fees, merchandise processing fees, and full baseline duties on every single consignment.

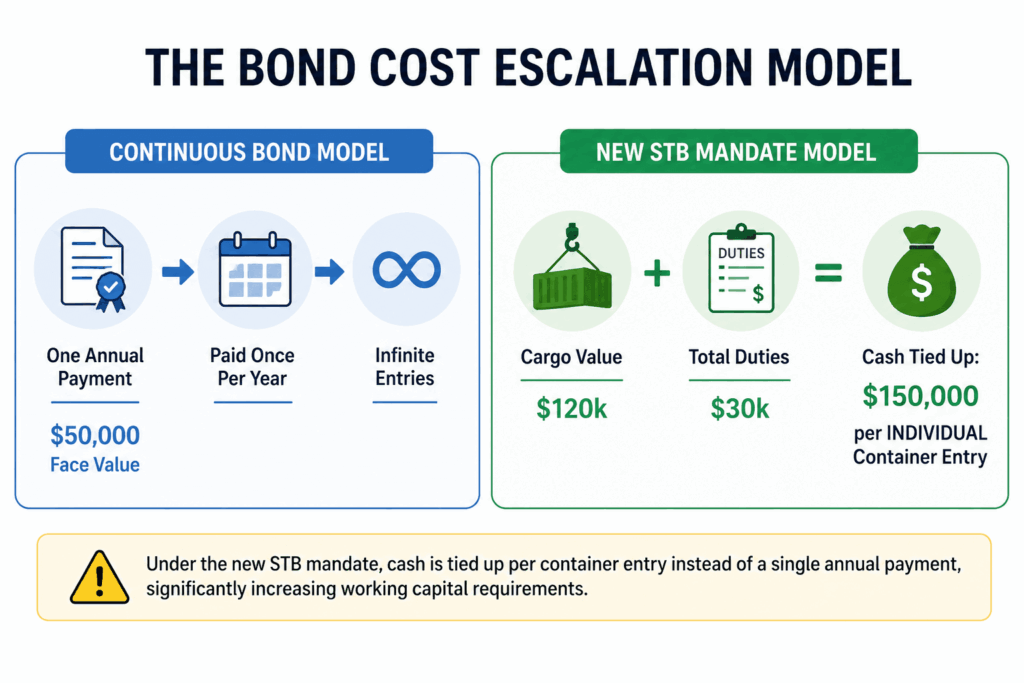

II. Systemic Restrictions on Continuous Customs Bonds

A Continuous Customs Bond is an annual financial instrument with a standard face value starting at $50,000 that covers 10% of all duties, taxes, and fees paid by an importer over a rolling 12-month cycle. Under the new executive order, CBP is instructed to issue a blanket denial of Continuous Bonds to foreign-registered importers unless they secure explicit, highly rare administrative exemptions.

Instead, foreign entities must now purchase a Single Transaction Bond (STB) for every individual container or air shipment they clear through U.S. ports.

- An STB must typically be written for a value equal to the full entered value of the cargo plus all applicable duties, taxes, and statutory fees.

- If the goods are subject to secondary government oversight (such as FDA, EPA, or DOT regulations), the STB value is routinely tripled.

For an enterprise managing a steady stream of China to US ocean freight, replacing a single annual $50,000 bond with dozens of individual Single Transaction Bonds creates an exponential spike in immediate cash outlay. It slows down processing timelines, and severely chokes working capital velocity.

III. Mandatory CTPAT Integration

The order decrees that any foreign entity attempting to execute a formal entry must either maintain a direct, fully certified CTPAT (Customs-Trade Partnership Against Terrorism) tier status or clear their shipments through a licensed U.S. customs broker who is actively CTPAT certified and assumes full financial co-liability for the cargo profile.

Because CTPAT certification requires exhaustive, end-to-end audits of physical factory security, data encryptions, warehouse access controls, and supply chain transparency, the barrier to entry for a standalone foreign seller has effectively become insurmountable.

4. The Sunset of “Shell” LLCs: Redefining True U.S. Importer Status

In anticipation of tighter regulations, many cross-border brands attempted to bypass foreign importer restrictions by setting up paper-only “Shell” Limited Liability Companies (LLCs) in states like Delaware, Wyoming, or Nevada. These entities frequently utilized a standard registered agent address, held no physical real estate, employed zero local staff, and maintained zero capital inside the United States.

The June 3 Executive Order explicitly terminates the validity of this practice. To qualify as a legitimate U.S. Importer of Record, an corporate entity must now conclusively prove it meets a strict checklist of real domestic presence:

- Substantive Commercial Footprint: The corporation must maintain a verifiable, brick-and-mortar office or an active, leased warehouse facility. P.O. Boxes, virtual business suites, and shared registered agent addresses are flagged by CBP automated risk-screening engines.

- Domestic Asset Backing: The entity must hold liquid capital, equipment, or physical inventory within U.S. borders that can be legally attached by federal courts in the event of trade fraud or duty default.

- Verifiable Executive Governance: The entity must be legally directed, operated, and controlled by verified U.S. citizens or legal permanent residents (Green Card holders) who bear personal legal liability for corporate trade infractions.

If your current US Amazon FBA logistics framework relies on a cheap, online-formed LLC with no actual physical operations in the United States, CBP’s new automated validation screening will rapidly reject your customs filings, locking your shipments in a state of indefinite administrative transit.

The Takeaway: That cheap $100 internet-formed “shell” LLC with a virtual mailbox is now useless. If there isn’t a physical office and a US resident holding personal legal liability, your customs entry will fail.

5. Customs Audit Weapons: Double-Invoicing Controls & The 50% Penalty Floor

The executive order arms CBP port directors with two severe regulatory enforcement mechanisms designed to root out valuation fraud and systemic under-declaration.

Mandatory Cross-Border Document Reconciliation

CBP now has the system capacity and legal mandate to require importers to submit official export-country customs declarations (such as the verified export manifests filed with China Customs – GACC) alongside the standard U.S. entry documentation.

This directly targets the widespread industry practice of double-invoicing. Historically, unscrupulous operators would generate a high-value invoice for Chinese export tax rebate processing, and a secondary, fabricated low-value invoice for U.S. customs clearance to evade ad valorem duties and Section 301 tariffs. If an audit reveals that the FOB value reported to China Customs does not perfectly match the entered value submitted to U.S. Customs, the entire shipment is subject to immediate structural seizure under 19 U.S.C. § 1592.

The 50% Minimum Penalty Floor

The order eliminates a significant portion of CBP’s historic discretionary power to mitigate and reduce financial penalties for first-time or non-willful trade infractions. It establishes a hard statutory minimum penalty floor of 50% of the domestic value of the merchandise for any material customs violation resulting from negligence or misdeclaration.

When a port director’s capacity to reduce fines is restricted by executive fiat, cargo line liquidations become immensely expensive. This leaves logistics providers with no viable path to negotiate or settle errors out of court.

6. Phased Implementation Timeline: The 90-180 Day Countdown

This executive order is an active, structural rollout with hard enforcement milestones mapped across the remainder of 2026 and heading into 2027.

THE 2026-2027 CUSTOMS COMPLIANCE TIMELINE

| Phase Target | Hard Regulatory Enforcement Action Implemented |

| Within 90 Days(By Sept 2026) | 1. Cross-border document cross-examination infrastructure goes live 2. Mandatory implementation of the 50% minimum statutory penalty floor. |

| 90 to 180 Days(By Dec 2026) | 1. Systematic deployment of the asset verification protocols for IORs. 2. Rollout of the real-time “Good Standing” importer rating network. |

| July 1, 2027 | Absolute global termination of the low-value de minimis exemptions. |

| Active Reality | Immediate cargo holds on unverified foreign consolidation manifests. |

While the complete administrative infrastructure is slated for phased integration over the coming months, the immediate chilling effect on air and ocean shipping lanes is already observable. Air freight small-parcel consolidations and mixed LCL (Less than Container Load) container manifests are experiencing unprecedented exam rates at primary entry hubs like Los Angeles, Long Beach, New York, and Chicago.

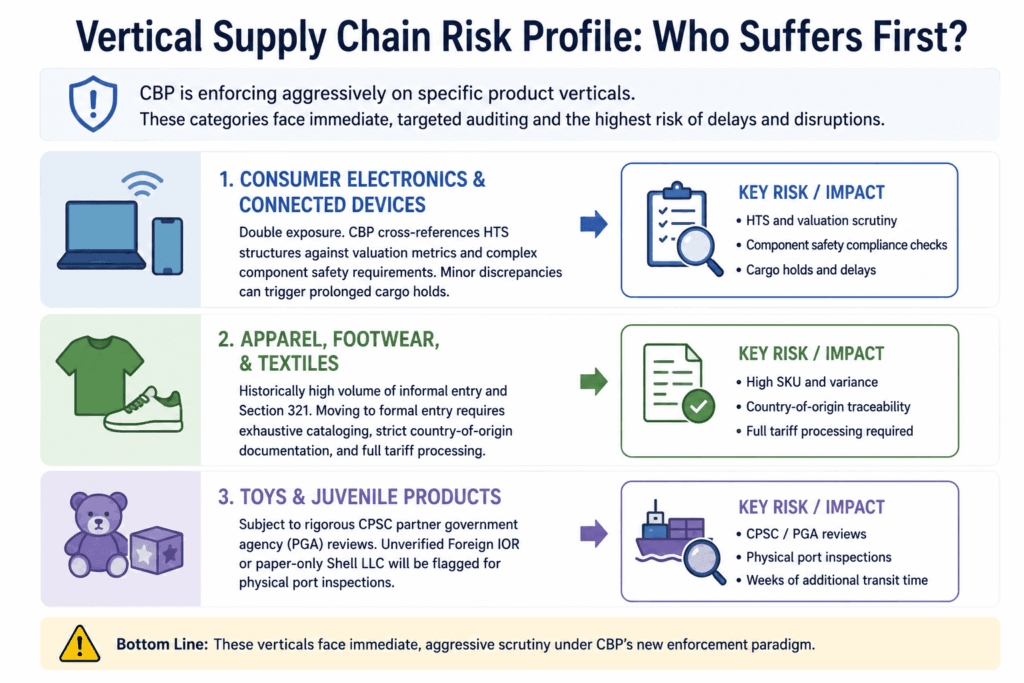

7. Vertical Supply Chain Risk Profile: Who Suffers First?

The impact of this enforcement paradigm is not uniform across all trade categories. Based on CBP’s stated enforcement priorities, specific product verticals are facing immediate, aggressive targeted auditing:

- Consumer Electronics & Connected Devices: If you are importing consumer tech, your supply chain is facing double exposure. CBP is cross-referencing your HTS structures against both valuation metrics and complex component safety requirements. Any minor discrepancy in your clearance profile can trigger prolonged cargo holds. To understand how these customs changes interact with the complex documentation requirements for battery-powered products, consult our comprehensive guide on [The 2026 Dangerous Goods Document Blueprint: Demystifying UN38.3, MSDS, and Customs Compliance].

- Apparel, Footwear, and Textiles: This sector historically represents the highest volume of informal entry and Section 321 processing. Shifting these high-SKU, high-variance products to formal entry models requires exhaustive cataloging, strict country-of-origin trace documentation, and full tariff processing.

- Toys and Juvenile Products: Subject to rigorous Consumer Product Safety Commission (CPSC) partner government agency (PGA) reviews. Under the new guidelines, an unverified Foreign IOR or a paper-only Shell LLC will be systematically flagged for physical port inspections, adding weeks to standard transit timelines.

8. Strategic Pivots: Transitioning to a Compliant B2B Import Framework

The era of relying on non-compliant “all-inclusive tax/duty clearance” channels to handle your Amazon FBA shipping is officially over. To protect your brand’s market equity, inventory velocity, and cash flow, you must migrate your customs infrastructure toward an authentic, structurally sound B2B framework.

Step 1: Re-Engineer Your Importer Architecture

Audit your current customs entry profiles immediately. If your freight forwarder is utilizing a generic, multi-client importer code or an offshore entity lacking domestic backing, you must immediately transition to an authentic, capitalized U.S. corporate consignee structure.

Step 2: Ensure Strict Valuation Transparency

Ensure your commercial invoices reflect accurate, defensible valuation methodologies (such as the actual transaction value paid to the manufacturer). Your bookkeeping must maintain a clean, unbroken paper trail that perfectly links your domestic U.S. bank payments, purchase orders, factory receipts, and international customs declarations.

Step 3: Align with CTPAT Certified Supply Chain Partners

Only route your commercial cargo through logistics networks whose partner customs brokers hold active, verified CTPAT certifications. This integration serves as a critical compliance cushion, lowering your statistical risk score within CBP’s automated targeting systems and minimizing unnecessary terminal cargo holds.

How Kisun Shipping Insulates Your Supply Chain from Enforcement Disruptions

In a high-scrutiny regulatory environment, choosing a logistics provider is no longer just about finding the lowest spot rate on an ocean lane. It is about protecting your enterprise from catastrophic compliance penalties.

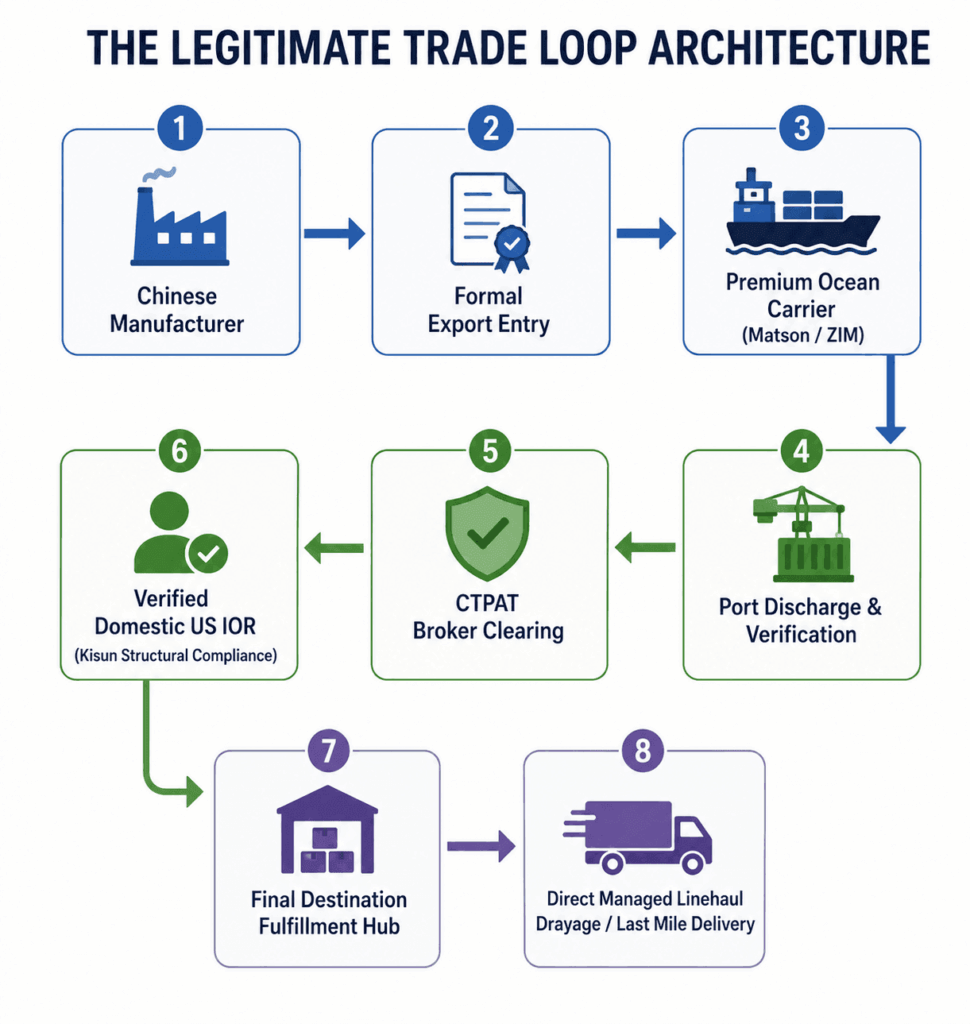

At Kisun Shipping, we don’t rely on gray-market consolidation loops or vulnerable foreign importer networks. We provide a fully integrated, highly compliant B2B trade infrastructure designed to withstand intense federal oversight:

- Legitimate Domestic Import Solutions: We provide our clients with access to verified, fully capitalized U.S.-based importer frameworks equipped with robust Continuous Bonds and clear domestic operating assets.

- Tier-1 CTPAT Broker Integration: Every customs entry processed through the Kisun network is executed by highly vetted, CTPAT-certified customs brokers who enforce rigorous KYC compliance from day one.

- End-to-End Operational Control: From the moment your cargo leaves the manufacturing plant in China to its formal clearance and final linehaul delivery at domestic logistics hubs, we maintain complete visibility over your supply chain.

Unverified customs documentation and non-compliant clearing models can quickly lead to costly port delays and cargo liquidations. If you are uncertain whether your current corporate structure or forwarder’s customs framework complies with the June 3 Executive Order, Connect with a Kisun Shipping Compliance Specialist Today to request an audit of your import framework.

For a deeper analysis of how these tightening customs regulations can affect your transit timelines and terminal processing speeds across major West Coast and East Coast trade lanes, read our comprehensive operational evaluation on [An In-Depth Analysis of US Ocean Freight: How to Choose Between Matson, ZIM, and Standard Carriers].

China Logistics Expert

About the Author

Katherine Kang is a China-based logistics consultant with over 11 years of experience in international trade and freight forwarding. Specializing in helping SMEs import from China to the USA, Canada, and Europe, she focuses on compliant, cost-effective solutions to avoid delays, tariffs, and hidden fees. From anti-dumping guidance to CNY planning, Katherine has managed hundreds of shipments, saving clients 15-30% on average.

Connect with Katherine on LinkedIn or contact Kisun Shipping for a free import consultation.