July 2026 China Ocean Freight Forecast: Why New Suez Surcharges and Panama Drought are Triggering Another Massive Rate Spike

If you thought the punishing ocean freight rate hikes in June were just a temporary market blip, it is time to reassess your Q3 and Q4 import budgets.

As we head deeper into June 2026, the global shipping ecosystem is entering a prolonged phase of severe operational disruption. For international importers orchestrating shipping from China, any baseline logistics projections established earlier this spring are officially obsolete. The Shanghai Containerized Freight Index (SCFI) has already blasted past the 2,572-point threshold—marking a staggering 34.55% month-on-month velocity spike—and spot rates are catching up to historical peak crisis levels.

Just as supply chain managers hoped for a pre-summer stabilization window, fresh regulatory, climatic, and geopolitical shocks have converged on the world’s two critical maritime arteries: The Suez Canal and The Panama Canal.

THE JULY 2026 OCEAN FREIGHT DISRUPTION MATRIX

| Maritime Chokepoint | Hard Regulatory/Climatic Shift | Direct Supply Chain Impact on Importers |

| Suez Canal (Egypt) | 12% Container Surcharge Spike (Effective July 15, 2026) | Erases routing profitability; forces permanent Cape of Good Hope diversions. |

| Panama Canal | Draft cut to 49.5 feet (Effective July 1, 2026) | Neopanamax vessels forced to shed weight; drops hundreds of USEC TEUs per voyage. |

| Transpacific Lanes | Massive Carrier GRI Push (Effective July 1, 2026) | COSCO mandates $3,000/FEU general rate increases across all US/Canada ports. |

As an international importer, you cannot afford to look at these developments as distant maritime news. They are the exact macro-catalysts that ocean carriers are leveraging to implement sweeping General Rate Increases (GRIs) for July.

Below is an unvarnished operational audit of why China ocean freight rates are on a non-negotiable upward trajectory for July 2026, and how you can shield your inventory from terminal delays.

The July 1 Shockwave: Decoding the Monster General Rate Increases (GRI)

To understand how rapidly the ocean freight market is tightening, you only need to examine the pricing frameworks filed by Tier-1 carrier alliances for July 1, 2026.

Led by aggressive capacity management strategies, ocean liners are systematically removing vessel space from major trade loops to keep space utilization indexes near 100%. COSCO Shipping Lines recently laid down an aggressive blueprint for the Transpacific trade lane, confirming a massive July 1 GRI for all U.S. and Canadian destinations:

- US$2,400 per 20-foot standard container (TEU)

- US$3,000 per 40-foot standard container (FEU)

- US$3,375 per 40-foot High Cube container

- US$3,798 per 45-foot specialized container

This GRI applies universally across all entry pathways—whether your cargo is routed via U.S. West Coast local ports, U.S. East Coast all-water loops, or complex Gulf Coast intermodal networks. When Tier-1 carriers push a $3,000 baseline adjustment on a single 40ft slot, it signals that the broader structural conditions supporting elevated China export freight trends are locked in through at least October.

The Bottom Line: Any Q3 import pricing matrix built on freight rate assumptions from before March 2026 is currently underestimating your landed container costs by 30% to 50%. If you do not lock in space allocations now, you will be priced out of the peak shipping season entirely.

Factor 1: The Suez Canal Transit Fee Hikes (Effective July 15)

The primary operational trigger behind the upcoming mid-July volatility comes directly from the Suez Canal Authority (SCA) in Egypt. In a series of navigational circulars issued on June 7, 2026, the SCA announced a sweeping increase in its “Temporary Surcharges” across almost all commercial vessel classes, slated for July 15, 2026.

While the mainstream media is heavily focused on the steep cost escalations hitting crude oil tankers (surcharges jumping from 25% to 37%) and dry bulk carriers (more than doubling from 10% to 22%), international retail and e-commerce importers must focus on the container line metrics. The SCA has confirmed a uniform 12% surcharge adjustment for container ships, applied on top of their standard baseline transit dues and existing deck-tier container fees.

SUEZ CANAL AUTHORITY JULY 15 SURCHARGE ESCALATION

| Laden Crude Oil Tankers | Surcharge jumps from 25% to 37% (+12% Net) |

| Dry Bulk Carriers | Surcharge escalates from 10% to 22% (+12% Net) |

| Commercial Container Ships | 12% Surcharge enforced on top of base dues & deck-tier fees |

The Cascading Capacity Crunch:

The SCA is executing this price adjustment at a time when regional military flashpoints are re-igniting. Fresh missile exchanges in the Middle East have prompted regional militant factions to declare a total ban on specific commercial vessels operating in the Red Sea corridor.

For international brands importing from China, this creates a devastating compounding effect:

- The Cape of Good Hope Premium: Carriers who continue to bypass the Red Sea by routing around the Cape of Good Hope consume an extra 10 to 14 days of transit time per voyage. This diversion burns immense amounts of bunker fuel and effectively traps thousands of empty containers at sea, starving Asian export hubs of equipment.

- The Suez Transit Tax: For the liner companies attempting to maintain Suez transits to hit tight schedules, the new 12% SCA surcharge—combined with soaring war risk insurance premiums—makes the route extraordinarily expensive.

Carriers will not absorb these multi-million-dollar operational surcharges. They are already translating these canal fee hikes directly into your booking sheets via Emergency War Risk Surcharges and Peak Season Surcharges (PSS).

In Short: Whether your vessel chooses to transit the Suez Canal or sail around Africa, the carrier’s operational cost is skyrocketing. That financial burden is being passed entirely to the shipper via your July freight bill.

Factor 2: The Panama Canal Climate Bottleneck (Effective July 1)

While the eastern hemisphere grapples with geopolitical and regulatory surcharges, the western hemisphere’s primary maritime shortcut is facing a severe climatic bottleneck.

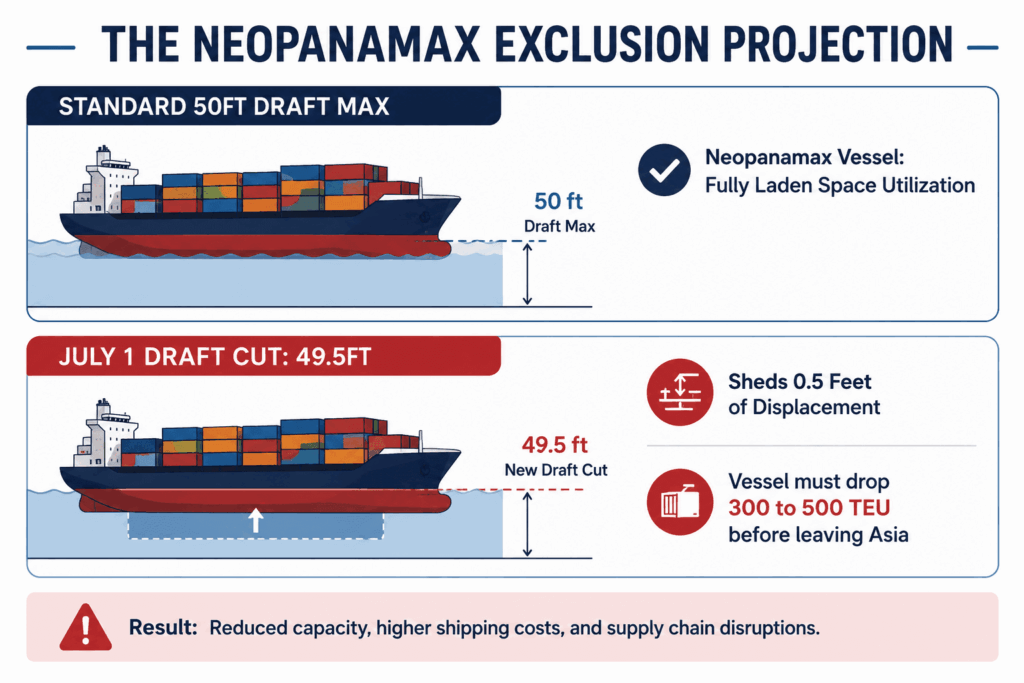

The Panama Canal Authority (ACP) issued an official advisory confirming that despite strong historical traffic volumes earlier in the year, it will officially reduce the maximum allowable draft for the Neopanamax Locks to 49.5 feet (15 meters), effective July 1, 2026. This represents a 0.5-foot structural drop from the previous 50-foot baseline.

The reason behind this sudden intervention is an aggressive climatic shift. Meteorological forecasting data from the U.S. National Oceanic and Atmospheric Administration (NOAA) indicates that Pacific trade wind anomalies and warming sea temperatures have made a powerful El Niño climate cycle virtually certain for the latter half of 2026. Models predict the intensity of this cycle could match the severe “Super El Niño” disruptions of 2015/2016, far exceeding the drought conditions encountered during the recent 2023/2024 shipping crisis.

The Physics of the Transpacific Rate Spike:

A 0.5-foot reduction in permissible draft sounds minor to an outsider, but in the world of heavy ocean freight, it forces a massive physical compromise:

- To maintain a safer, shallower displacement when entering Gatun Lake, large Neopanamax container vessels must shed significant weight.

- In practical terms, a 0.5-foot draft restriction forces a standard 14,000 TEU vessel to leave approximately 300 to 500 containers behind on the docks in China per voyage.

Because these vessels cannot travel across the Pacific at full payload capacities, the per-container operational cost for the remaining slots surges exponentially. This directly triggers container rolling at major Chinese ports like Shanghai, Ningbo, and Shenzhen. If your cargo is booked on a standard all-water service heading to the U.S. East Coast (USEC), you are now competing for a radically shrinking pool of available slots.

The Reality: The Panama Canal draft restriction means less capacity per vessel heading to the East Coast. Less capacity means skyrocketing spot rates. If your cargo is heavy or oversized, expect immediate port delays unless your forwarder has priority allocation.

Factor 3: The Collision of Peak Season and New Trade Policies

Compounding these dual canal crises is a massive influx of front-loaded inventory. Importers across North America and Europe are aggressively accelerating their Q3 and Q4 ordering cycles to stay ahead of two major logistics threats:

- Peak Season Compression: Major global brands are pulling their holiday inventory shipments forward into June and July to ensure products hit store shelves well before the autumn logistics rush.

- The New US Customs Matrix: Importers are scrambling to secure vessel space to clear their inventory before tightening trade policies create severe bottlenecks at domestic ports. With the recent implementation of aggressive executive guidelines targeting import frameworks, the margin for error in customs clearance has dropped to zero.

To explore how these new federal guidelines are permanently changing the legal and financial liabilities for international brands, read our exhaustive compliance breakdown on The Death of Gray-Market DDP: Decoding Trump’s June 3 Executive Order on US Customs Enforcement and the New Foreign IOR Restrictions

This influx of early peak-season volume is colliding with a global fleet that is already structurally out of position due to the Suez reroutings. The result? A perfect storm of blank sailings, equipment shortages, and immediate container spot rate spikes.

Strategic Insulation: How Importers Can Survive the July Rate Spikes

Navigating this volatile environment requires moving away from transactional, spot-market shipping strategies. If you simply book your cargo with the cheapest forwarder on a week-to-week basis, your containers will likely be rolled repeatedly, leading to catastrophic stockouts.

To stabilize your supply chain velocity through the July 2026 volatility, implement these three operational pivots immediately:

A. Diversify Routing Pathways via the U.S. West Coast

With the Panama Canal restricting Neopanamax drafts and driving up all-water rates to the East Coast, routing your cargo via U.S. West Coast gateways (USWC) and utilizing domestic intermodal rail or transloading networks is highly strategic. This approach completely bypasses the Panama bottleneck and shaves weeks off your end-to-end transit times.

B. Leverage Premium Express Ocean Channels for High-Value SKUs

For your high-velocity, time-sensitive SKUs or your critical US Amazon FBA shipping inventory, cease gambling with standard, low-cost alliance vessels that are highly vulnerable to port congestion and container rolling. Instead, allocate a dedicated percentage of your volume to premium express services like Matson (CLX) or ZIM (ZEX).

To understand the structural advantages of these premium channels—such as Matson’s private C60 terminal access and dedicated chassis deployments—review our operational audit on An In-Depth Analysis of US Ocean Freight: How to Choose Between Matson, ZIM, and Standard Carriers

C. Factor in the Last-Mile Delivery Bottleneck

When calculating your transit timelines through the July peak, remember that port discharge is only half the battle. If your final delivery destination requires moving heavy or oversized cargo across the country via domestic truck networks, a fast boat will not save a poorly planned domestic leg. Always confirm with your logistics provider whether your final leg relies on fragmented Less-Than-Truckload (LTL) assets or dedicated express trucking networks to ensure your port-side speed advantages aren’t diluted.

Frequently Asked Questions

Q1: Will ocean freight rates from China continue to rise in July 2026?

A: Yes, most routes are expected to remain firm or rise further in July. The combination of Panama Canal draft restrictions, new Suez Canal surcharges starting July 15, and ongoing Red Sea risks is keeping capacity tight and costs elevated.Q2: How much will the Panama Canal restrictions affect my shipments?

A: Starting July 1, the maximum draft for Neopanamax vessels will be reduced to 49.5 feet. This may force some vessels to carry less cargo or result in more transshipment, potentially adding delays and slight cost increases, especially for US East Coast and Midwest shipments.Q3: What are the new Suez Canal surcharges effective July 15?

A: The Suez Canal Authority has increased temporary surcharges for most vessel types. Dry bulk carriers see the biggest jump (from 10% to 22%), while crude tankers, LPG carriers, and others also face notable increases. Container ships maintain a 12% tiered surcharge.Q4: Which routes from China are most affected in July 2026?

A: Europe and Mediterranean routes are seeing the strongest pressure due to Suez surcharges and Red Sea avoidance. US West Coast remains elevated but relatively more stable, while US East Coast and Middle East routes (including Saudi Arabia) face additional challenges from canal adjustments and war risk factors.Q5: Should I book July sailings now or wait?

A: It’s generally better to book earlier rather than later. Space on premium services (Matson, ZIM) is tightening, and waiting may result in higher rates or rolled cargo. For non-urgent shipments, consider securing standard carrier space with extra buffer time.Q6: How should Amazon FBA sellers adjust their shipping strategy?

A: FBA sellers should prioritize reliable services like Matson or ZIM for urgent replenishment to protect rankings. For regular stock building, a mix of ZIM and standard carriers with sufficient buffer (at least 35–45 days) is recommended to balance cost and reliability.Q7: Will these changes affect shipping from China to Saudi Arabia?

A: Yes. Suez-related surcharges and Red Sea risks directly impact Middle East routes. Expect higher war risk insurance and potential delays. We recommend early booking and confirming SFDA/SABER documentation well in advance.Q8: What is the smartest way to control shipping costs right now?

A: Diversify your carriers, book space 4–6 weeks ahead, compare all five major Chinese ports, and calculate total landed cost (not just ocean freight). Working with an experienced forwarder who can access multiple options in real time is one of the best ways to manage this volatility.Secure Your July Space Allocations with Kisun Shipping

The global maritime market is entering an era defined by structural capacity shortages and rapid, volatile cost adjustments. In this environment, an experienced, proactive logistics partner is the single most important asset for your business.

At Kisun Shipping, we actively monitor global maritime chokepoints, carrier GRI filings, and shifting port regulations in real time. We don’t just hand you a standard quote sheet; we construct resilient, multi-tiered supply chain portfolios engineered to keep your goods moving when global supply chains tighten.

Through our direct contracts with Tier-1 ocean liners, premium fast-boat networks, and CTPAT-certified customs brokers, we provide stable, reliable space allocations and highly compliant customs clearance pathways across every major U.S. and Canadian port of entry.

The July 2026 rate spike is no longer a prediction—it is actively transforming global trade. If you want to audit your current space allocations, evaluate alternative USWC transloading pathways, or secure predictable pricing structures for your Q3 inventory, Connect with a Kisun Shipping Allocation Specialist Today

China Logistics Expert

About the Author

Katherine Kang is a China-based logistics consultant with over 11 years of experience in international trade and freight forwarding. Specializing in helping SMEs import from China to the USA, Canada, and Europe, she focuses on compliant, cost-effective solutions to avoid delays, tariffs, and hidden fees. From anti-dumping guidance to CNY planning, Katherine has managed hundreds of shipments, saving clients 15-30% on average.

Connect with Katherine on LinkedIn or contact Kisun Shipping for a free import consultation.